China’s economic trajectory is decoupling from the U.S.

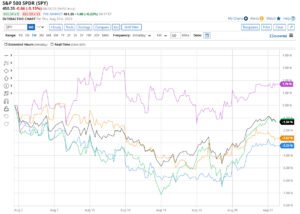

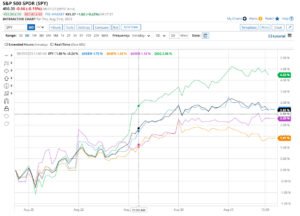

S&P 500 and the Nasdaq 100 Indexes closed the month basically flat, down around 1%. With gains being made over this week, in particular the QQQ up 4.2%. The Energy sector saved the indexes in August, up 1.7%. Without the energy trade the returns on the S&P 500 would have been even lower. The issue now is how long will the Energy trade last, after all it is a bet on the oil price. The S&P 500 Index (SPY) Thursday closed -0.16%, and the Nasdaq 100 Index (QQQ) closed +0.25%.

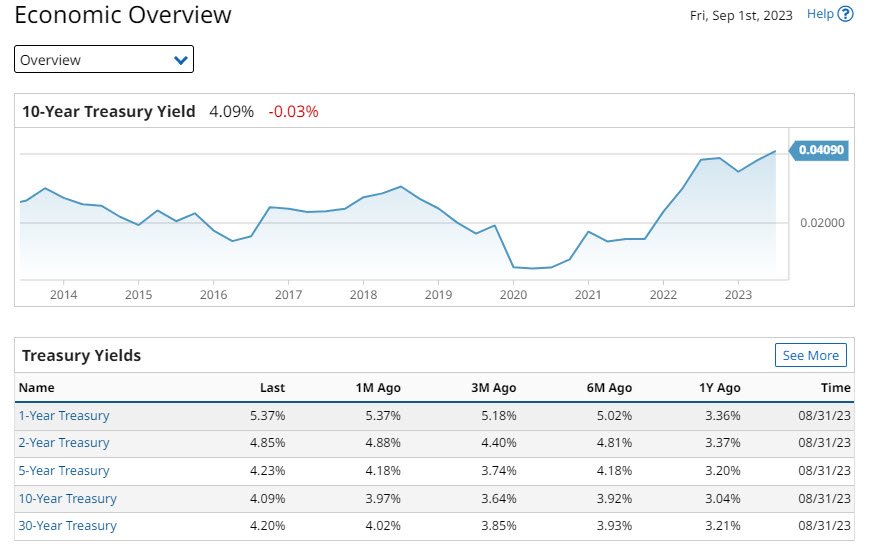

Inflation Data released did little to change things as the U.S. PCE deflator fell to a new post-pandemic low of +2.1 % (+2.9 % core). One of the key drivers into 2024 will bond yields at the long-end. Yesterday’s 0.06% drop in the 10-year T-note yield helped stocks. The stock market heading into 2024 will be extremely sensitive to bond yields. The July PCE deflator data of +3.3 % was up from the two years plus figure released in June.

June’s reading of +3.0 % remained well below the four-decade high of 7.0 % achieved in June 2022. The July core PCE deflator of +4.2 % was up from but well below the four-decade high of +5.4% in February 2022. The July PCE deflator fell to a new post-pandemic low of +2.1 % on an annualized basis. The core deflator fell to a new post-pandemic low of +2.9 %.

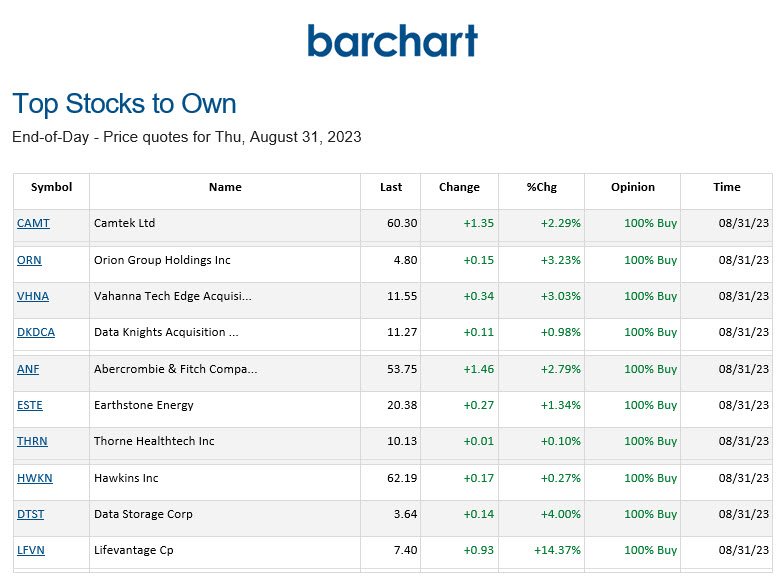

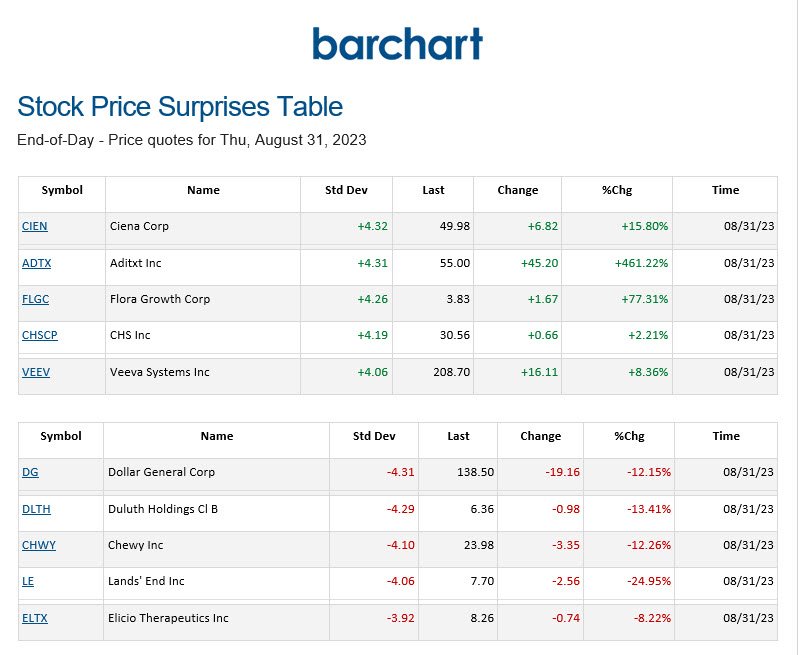

![]() surprises both upside and downside.

surprises both upside and downside.

![]()

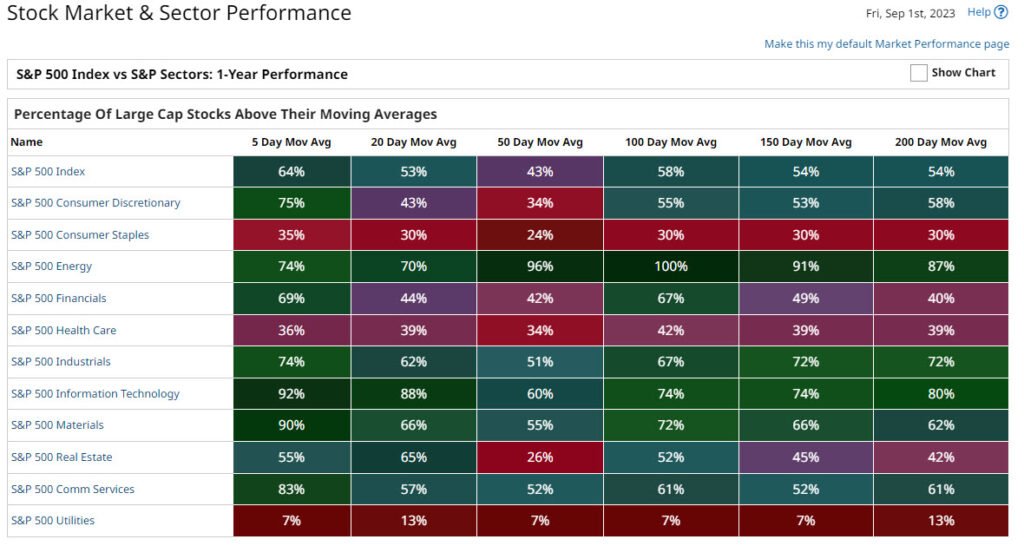

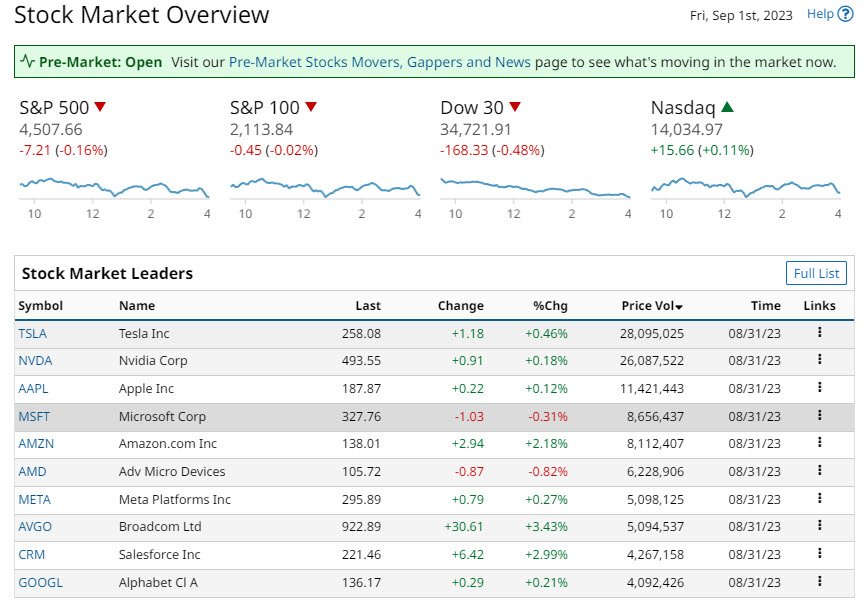

The charts used in this Blog Post are from Barchart. Barchart is a financial data and technology company that provides financial market data, news, analysis, and trading solutions.