March madness is usually college basketball – this time the banks

March Madness is usually associated with college basketball. Congratulations to all the teams and the winners, UConn men’s and LSU women’s. The unusual edition of March madness in 2023 came to the bank sector. The collapse of Silicon Valley Bank started the turmoil.

This event on March 10 was the second largest in U.S. history. It didn’t stop there. The fear was real, and the contagion effect led to the collapse of a couple of other banks. Then there was the big one, Credit Suisse, and the 167-year history consumed by USB over a weekend in March.

To test your knowledge, do the Quiz based on this blog, please click HERE.

bank’s edition of March Madness

So, what led to the bank’s edition of March Madness? Then what did Q1 2023 results last week say? The collapse of the three banks in the U.S. and the long overdue demise of Credit Suisse. Were they related, and what happened? In U.S. banks, the core problem was, as usual, the assets, but not the usual culprit being bad loans.

No, it was classic interest rate mismanagement. SVB invested in U.S. treasuries, and as interest rates rose, these bonds lost value. This was something any well-run bank and the regulators should have noticed. Then managed the issue. It wasn’t. The “Accounting Fix” needs a fix. For more information, please click HERE.

in the bank, where it is safe

The combined collapse of these banks added a lot of heat to the conversation. Why? Is your money safe in the bank? One thing we all have in common is that we all have banking relationships. Our banking relationship is one of our most sensitive. The events of the past couple of months combined with the events to come. They are and will emphasise the following premise. The whole banking system is based on the promise that depositors leave their money in the bank, where it is safe.

In reality, the contract in place is this. Above USD 250,000, you are an unsecured lender to a highly leveraged shop and receive a meager return. In a Bankruptcy Court, a depositor will stand in line with all other creditors. All are above-listed shareholders and Tier 1 bond holders. The arrangement to bail out Silicon Valley Bank depositors, all of them. Bar none. In effect, this action sets a precedent for making good on all deposits in the U.S.

Is this necessary to keep your money safe in the bank?

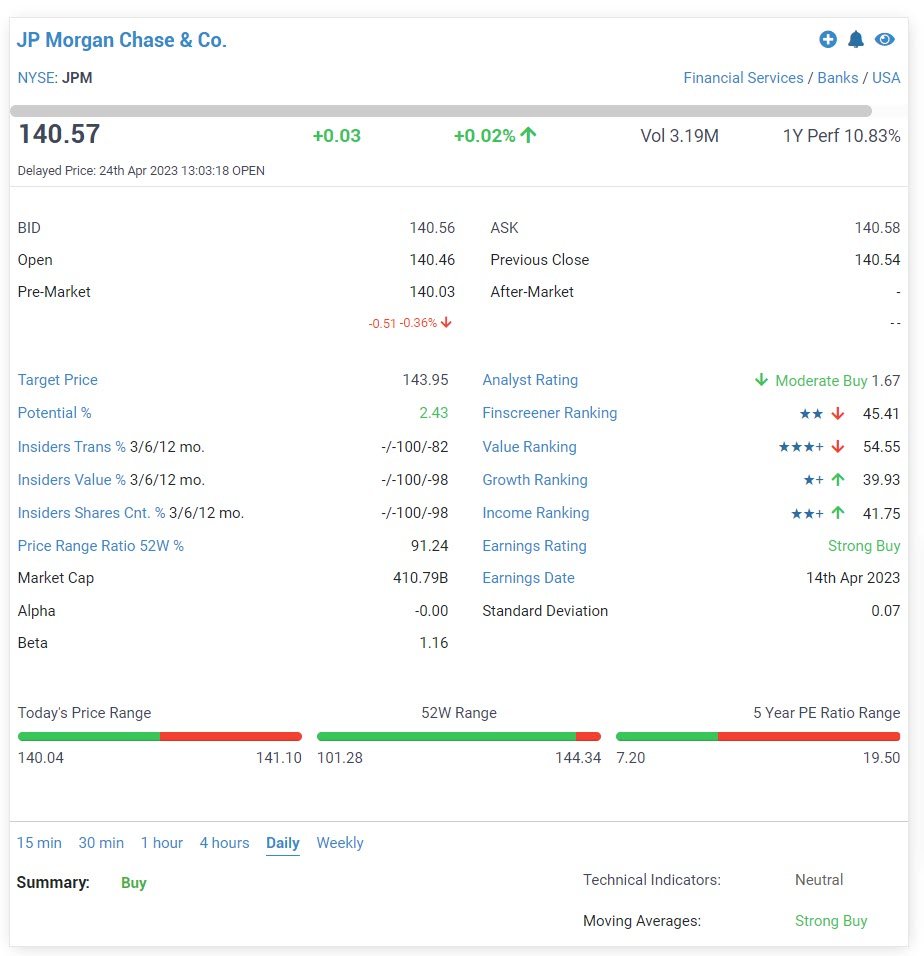

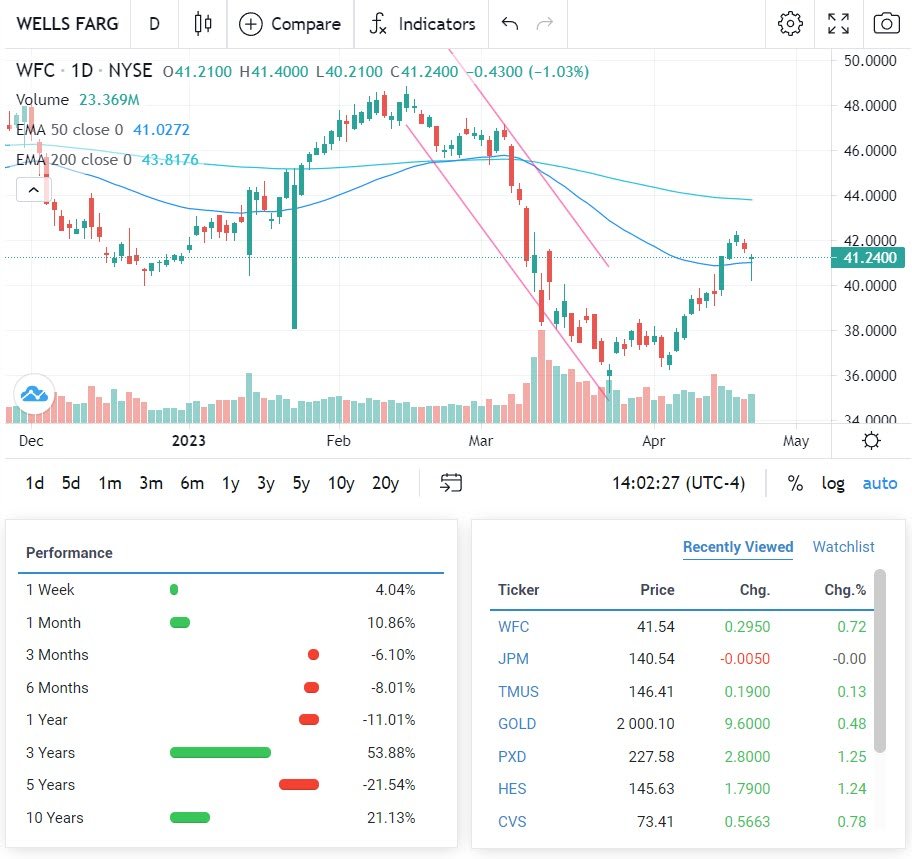

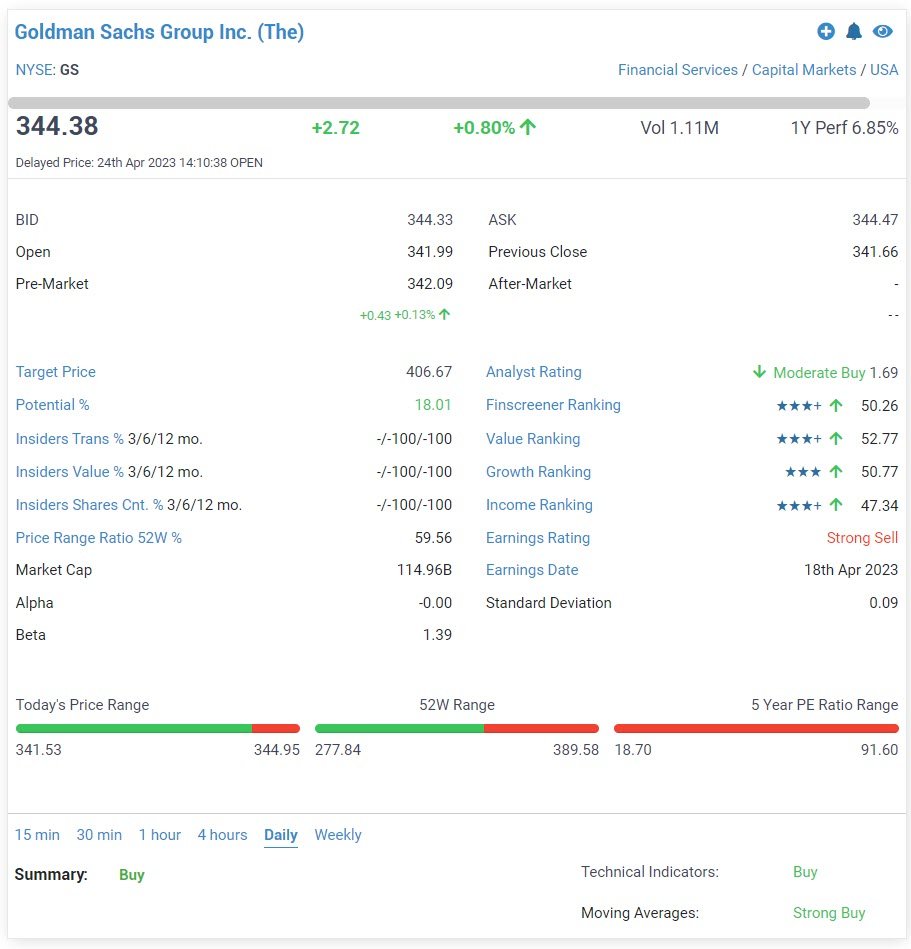

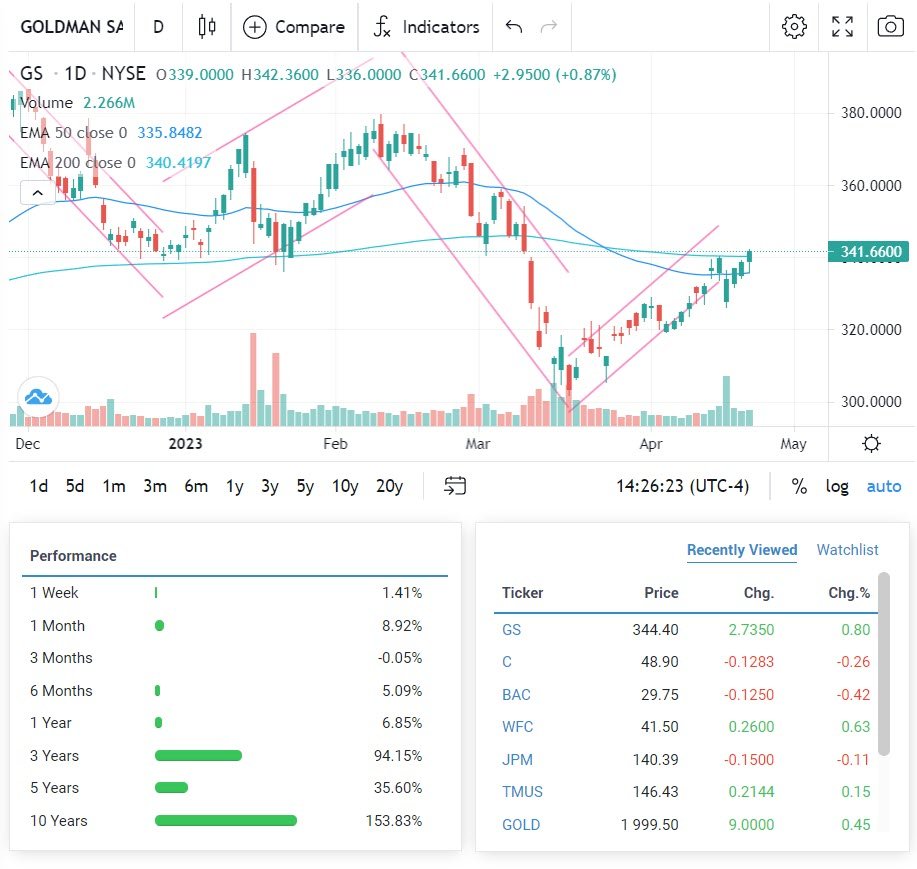

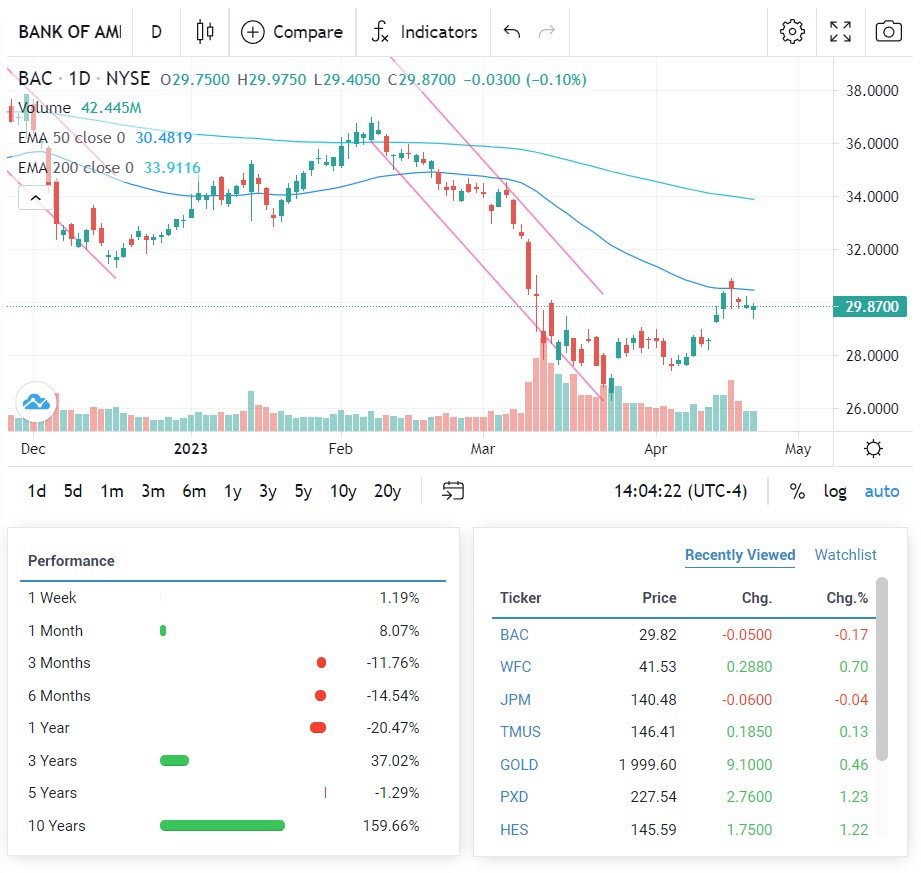

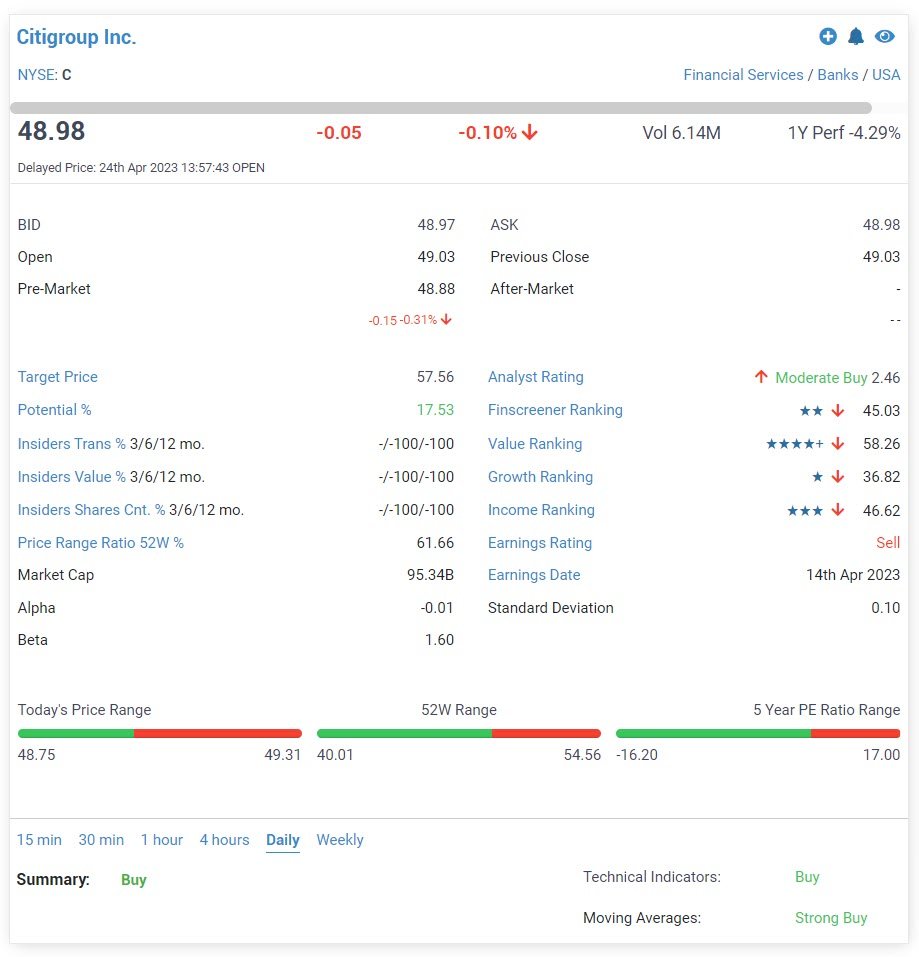

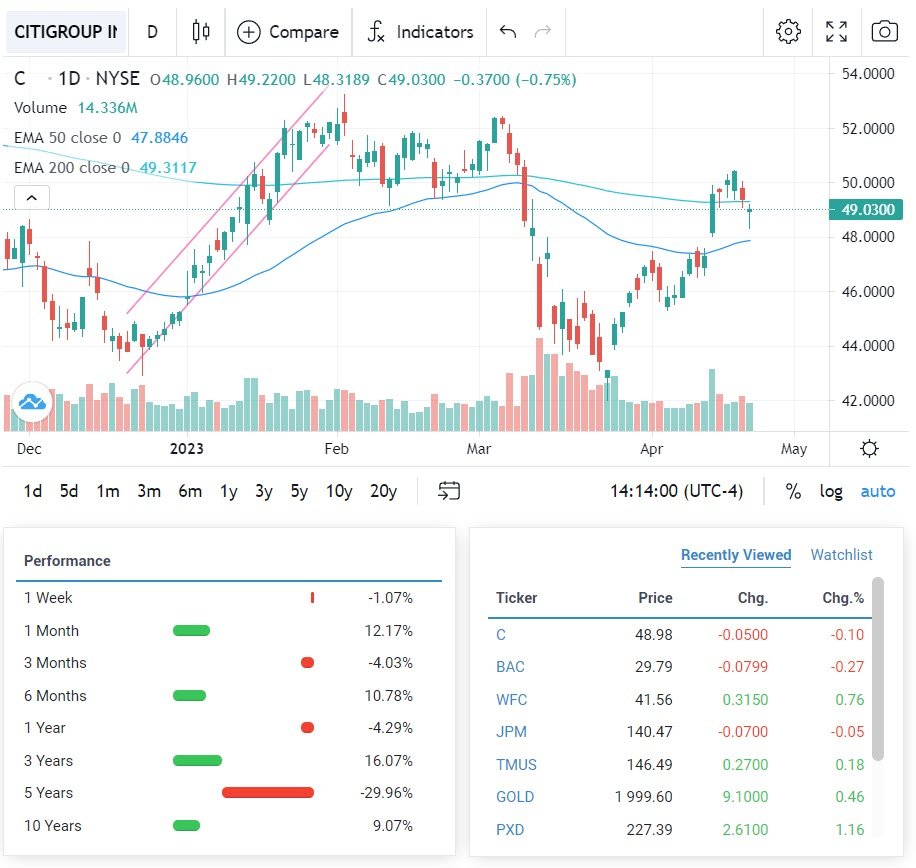

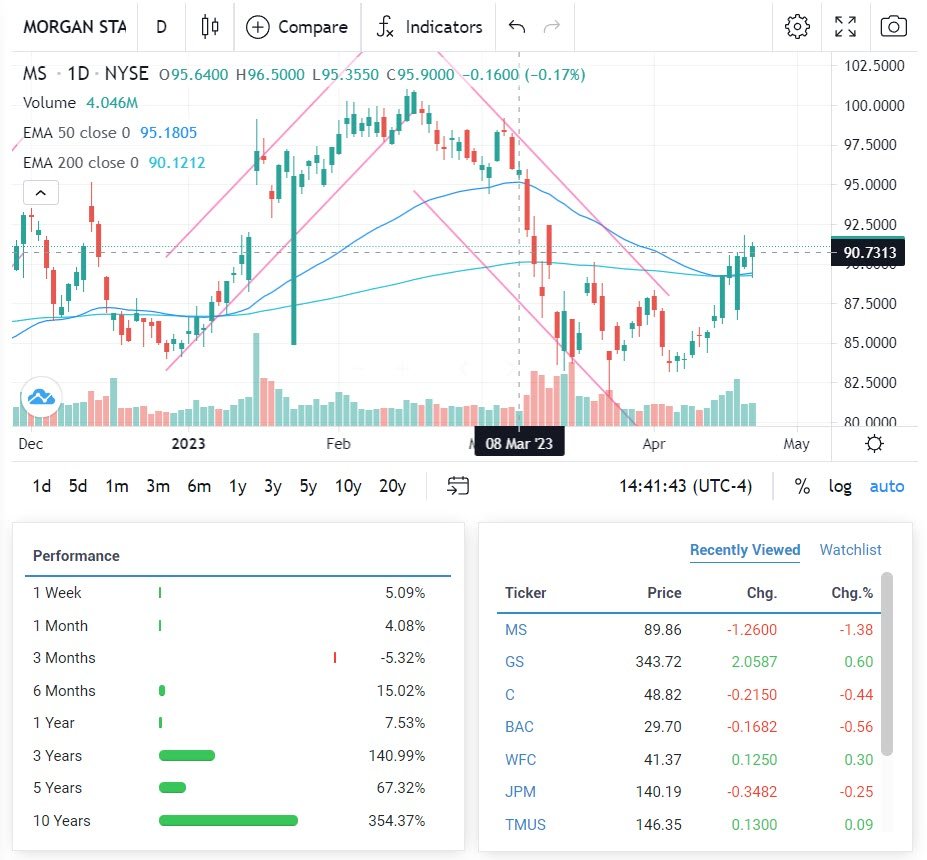

The Major U.S. Banks Earnings Reports

Let’s take a look.